Will City pass the FFP test? Part 2

Notes

Note 1: Gate Receipts

Although there is a limit to the growth potential of ticket sales, I have assumed a 10% year on year increase in Gate Receipts (additional Champions League Gate Receipts are shown separately in Note 3).

Note 2: TV Media

City's TV and Merit payment details are as follows.

TV/Media/Merit Payment

|

The 2010/11 are known figures (see link below). The 2011/12 figure of £60.6m is also confirmed in the second link. I have assumed City will receive £2m TV revenue for their Cup performances in 2011/2 (the £8.6m includes a £2m prize for winning the competition). The League payments pay to a fixed formula, so if we assume City win the League and the FA Cup in 2012/13, their TV and Merit income will be £52m (they are not in the Europa League and their Champions League receipts are detailed separately).

http://www.uefa.com/MultimediaFiles/Download/uefaorg/Finance/01/66/11/25/1661125_DOWNLOAD.pdf

Note 3: Champions League

City didn't get out of the Group stage in 2011/12 but I have projected that they reach the final in 2012/13. The figures are supplied by the Swiss Ramble page - see link below.

In addition to the Prize money, I have also added £750k for gate receipts for each of the 5 home games in 2011/12 and 8 if they reach the final in 2012/13.

| Champions League | 2011/12 | 2012/13 |

| Prize and TV (£m) | 18.2 | 46.4 |

| Additional Ticket and Commercial | 3.75 | 6 |

| 21.95 | 52.4 |

City would also receive additional commercial income in 2012 from their projected successful Champions League campaign. I have projected an additional £4m on top of the above figure.

http://swissramble.blogspot.co.uk/2012/04/champions-league-revenue-final.html

Note 4: Commercial Income

City have probably the most efficient Commercial team in the Premier League. I have generously projected that they continue to grow their Commercial income by 25% year on year. This would take their 2012/13 Commercial income up to around £101m (from £64.7m in the year they finished third and won the FA Cup).

Note 6: Etihad Deal

The Etihad deal is worth around £35m a year for 10 years. UEFA are still to review this deal to ensure it was transacted at a 'fair value'. However, I have assumed that they don't adjust the contract and also assumed that the deal is not front-end-loaded (if it were, then UEFA's view on the deal might be different).

Note 7: Nike deal

The new Nike deal does not commence until the 2013/14 season so has no positive effect in the first FFP Monitoring Period.

Note 8: Wages

Annual Accounts confirm the players sold and recruited after the 31 May 2010/11 account cut off. Wages increased by £2.5m as a result.

| Left | Wages wk | Wages Year |

| Boetang | £85,000 | £4,420,000 |

| Given | £80,000 | £4,160,000 |

| Jo | £80,000 | £4,160,000 |

| Bellamy | £90,000 | £4,680,000 |

| Caicedo | £65,000 | £3,380,000 |

| Wright-Philips | £65,000 | £3,380,000 |

| £24,180,000 | ||

| Joined | ||

| Sergio Agüero | £185,000 | £9,620,000 |

| Gaël Clichy | £90,000 | £4,680,000 |

| Samir Nasri | £150,000 | £7,800,000 |

| Denis Suárez | £30,000 | £1,560,000 |

| Stefan Savić | £58,000 | £3,016,000 |

| £26,676,000 |

This projection assumes no more joiners or departures before 31 May 2013.

Note 9: Title-winning bonus

I have assumed a 10% bonus (as percentage of wages) to all players. This would also be paid in 2012/13 if they also win the title (as I have assumed).

Note 10: Other Expenses

This accounting entry includes Audit Fees, costs of consumables and all the other ongoing operating expenses of running a multi-million pound business. The expenses grew by 18% from 2009/10 to 2000/11(from 42.4m to 50m) reflecting the expanding nature of the business. I have assumed expenses grows by only 10% in 2011/12 and stays flat in 2012/13.

Note 11: Amortisation

This standard line in club accounts probably needs some explanation.

You never see a line in the Profit and Loss Account (P&L) for "transfer fees paid out" (although you might see this in the Notes). The P&L only ever displays 'Amortisation' and 'Profit/Loss from player sales'.

A player signed for £20m on a 4 year contract will have to be written-down/depreciated/amortised as an expense at the rate of £5m a year for each year of the contract (£20m/4=£5m). The purchase prices does therefore appear in the accounts but not in one year - it is spread evenly over the live of the contract. The FFP calculations look at the Profit/Loss that a club makes - hence we are also interested in the amount of amortisation.

The player's value will be depreciated (as an 'intangible fixed asset' usually) over the duration of the contract. After three years, the above £20m player will have a book value of £5m. If the player is sold at that time, the club's accounts will record a 'profit/loss on player sales' where the selling price differs to the book value at the date of sale.

The 2010/11 records an annual Amortisation figure of £83.8m. The notes to the accounts also helpfully tell us the six players joined the club and the six left. As we have a good idea of the purchase price and contract duration of the new players and the book value and can work out the amortisation rate of the departing players, we can calculate the new Amortisation figure (taking a 'top-down' approach).

By taking this approach we see that Amortisation has increased by £1.7m (from £83.8m to £85.5m):

| Left | Annual Amortisation rate |

| Boetang | £2,100,000 |

| Given | £1,584,906 |

| Jo | £4,500,000 |

| Bellamy | £4,097,561 |

| Caicedo | £1,155,556 |

| Wright-Philips | £2,125,000 |

| £15,563,022 | |

| Joined | |

| Sergio Agüero | £7,600,000 |

| Gaël Clichy | £1,750,000 |

| Samir Nasri | £6,250,000 |

| Denis Suárez | £204,000 |

| Stefan Savić | £1,500,000 |

| £17,304,000 | |

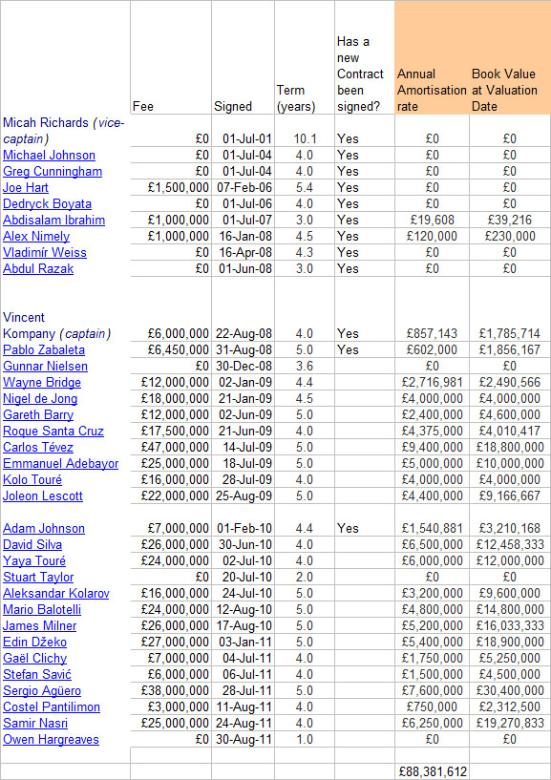

Interestingly, we can also come up with a similar Amortisation figure for next season if we itemise all the players on City's books and work out their individual book value and Amortisation rate. However this is less accurate as we often don't really know the true purchase price and contract duration (including any re-negotiated contracts for the whole squad).

However, I calculate that City's squad has book values and amortisation rates that look like this at 31 July 2012:

As you can see, my manually calculated Amortisation rate comes out to £88.4 (as oppose to the £85.5m in the more accurate top-down approach).

I have assumed that no new players are signed in 2012/13 (this is probably unlikely but will help us to track the impact on profitability).

Readers might find the book value figures of interest. Some players, such as Hart have been fully amortised and have a zero book value. If Hart were sold, all the proceeds would be accounted for immediately as a 'profit on player sales'- see note 14 below.

Note 12: Depreciation

The 2011/12 has been projected on a level basis.

Note 13: Profit on player sales

We know the players sold after the end of May 2010/11. By working out their book value at the date of sale, we can see that a £4.9 profit was received in 2011/12.

| Sale Price | Book Value at sale date | Profit/loss | |

| Boetang | £10,000,000 | £8,575,000 | £1,425,000 |

| Given | £3,500,000 | £3,433,962 | £66,038 |

| Jo | £6,500,000 | £5,625,000 | £875,000 |

| Bellamy | £0 | £4,439,024 | -£4,439,024 |

| Caicedo | £6,000,000 | £1,348,148 | £4,651,852 |

| Wright-Philips | £5,000,000 | £2,656,250 | £2,343,750 |

| Profit on sales | £4,922,615 |

I have assumed that no players are sold in 2012/13 (this is probably unlikely but it will help us to track the impact on profitability).

Note14: Exceptional items

I have assumed no Exceptional items. These often occur if, for example a manager is sacked and his contract is paid off. Technically the Amortisation figure for Bellamy shown in Note 14 should appear as an Exceptional Item in 2012/13 but for this exercise it is neater to show it within Profit/Loss on player sales.

Note 15: Chargeables

I have projected these on a level basis based on the 2011/12 figure.

Fair Play Exclusions/Limits

The Financial Fair Play limits are as follows (deficit values in euros - E45m is around £36m, E30m is around £20m).

Note 16: Other excludable items

Depreciation, finance costs and tangible fixed costs plus expenditure on youth team development. and community development activities can also be excluded from the FFP calculation. We know the depreciation and stadium lease charge from the accounts. It is not really possible to identify youth development and community development activities from the accounts but have again used the Swiss Ramblers estimates.

| Depreciation | 5.9 |

| Youth development | 10 |

| Community Development | 2 |

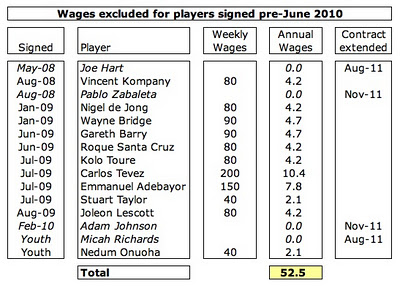

Note 17: Players signed before 1 June 2010

Players signed before 1 June 2010 can be excluded from FFP calculations for the 2011/12 season only. The wages can only be excluded if the pre-June wages are the only reason the club fails the FFP test (see my section on Annex XI). The wages are only excluded if the contract has not been re-negotiated.

Pre-June 2010 wages come to £53m (as identified by Swiss Ramble):

blog comments powered by Disqus