QPR's accounts released and heading for £50m fine

QPR’s controversial accounts were released this week. As anyone following this story will be aware, the club recently announced profits via a vague Press Release which claimed that surprisingly low losses of just £9.7m had been made in 2013/14. A number of people raised questions about how this could have been achieved without some accounting ‘slight-of-hand’ (see my previous article).

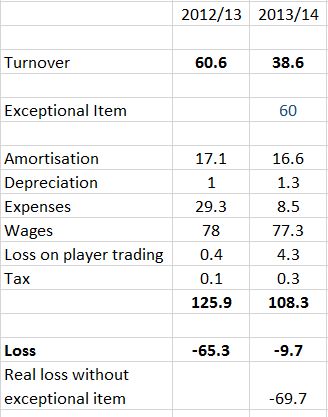

Now we have the accounts, it transpires that the club owners wrote off £60m in loans and classed this event as one-off income injection in the Profit & Loss account. If the £60m had been classified conventionally, the club would have reported a loss of £69.7m. The club accounts can be found here but the key events are summarised below:

The Exceptional Item is classified in the accounts as a Related Party Transaction (i.e. a transaction with the owner or someone connected to the ownership of the club). This makes it easier for the Football League to invoke their RPT rules. The FFP rules make it clear that this kind of transaction simply cannot be included in the Fair Play Calculation. Section 2.2.1 of the rules explains how such an item must be treated for FFP purposes:

.. a permanent and unconditional waiver of inter-company or Related Party debt must be treated as a capital contribution, as it results in an increase in equity;

Hence QPR are actually facing a ‘Fair Play Tax’ bill for somewhere around £50m. All this raises a number of questions about the way the accounts the way the club has portrayed events.

The original QPR Press release (here) seemed to have been written to suggest that the improved figures were in large part due to due to lower player costs (whereas in reality the wage costs and amortisation have improved by less than £2m). You have to wonder why the club tried to present events as they did.

The level of wages is interesting – essentially the club paid almost the same amount of wages in the Championship as they did in the Premier League (£77.3m). This is the highest level of wages ever paid by Championship club. OK, some of this figure (perhaps £5m or so) will relate to promotion bonuses but it is worth comparing QPRs wages to the approximately £13m wages paid by Derby –the club QPR defeated in the Play-off final. FFP constraints were brought in to help put a lid on wage escalation – however QPR almost seem to have felt they could play to a different set of rules.

The accounts themselves are also notable for the very thing they fail to mention: the £50m FFP fine. One would have thought Tony Fernandes Chairman’s Statement or the accountants or the auditors would have mentioned, at least in passing, a £50m fine? It is hardly small change and the fine is larger than last season’s turnover. If there is a juggernaut coming round the corner, the accounts should put you on notice – none of the professionals connected with pulling this document together have covered themselves in glory.

There is a potentially interesting detail in the way the £60m loan has been written off. QPR is owned 69% by a Tune QPR and 30% by Sea Dream. Tune QPR is owned by Fernandes, Maranun and Gnanalingam; Sea Dream is owned by the wealthy Mittal family. Of the £60m loan write-off, Mittal’s share was £5.6m or 11% of the amount written off. It is unclear why the write-off was structured in this way and it is possible that Tune QPR have agreed to be responsible for most of the debt.

Club debt now stands at £205m – despite the £60m loan cancellation, club debt has actually increased by around £5m.

blog comments powered by Disqus